.jpg)

When deciding how to protect your home and budget, understanding the difference between home insurance and home warranties is key. Here's a quick breakdown:

- Home Insurance: Protects against unexpected disasters like fires, theft, or storms. It's required by mortgage lenders and costs $1,200–$2,000 annually on average, with deductibles ranging from $500 to $2,500.

- Home Warranty: Covers repairs or replacements of systems and appliances due to normal wear and tear. It's optional, costing $540–$1,400 per year, with service fees of $75–$150 per visit.

Key Differences:

- Coverage: Insurance handles sudden damage (e.g., fire), while warranties cover gradual breakdowns (e.g., a failing HVAC system).

- Cost Structure: Insurance involves higher premiums and deductibles, while warranties offer predictable costs but frequent service fees.

- Claims: Insurance claims are for major losses, and warranties handle smaller, routine repairs.

Many homeowners use both for full protection. Insurance safeguards against big disasters, while warranties manage everyday repairs. Pairing them can minimize financial surprises.

Home Warranty vs. Homeowner's Insurance Explained: What Every Homeowner Needs to Know!

What Each Option Covers: Home Insurance vs. Home Warranty

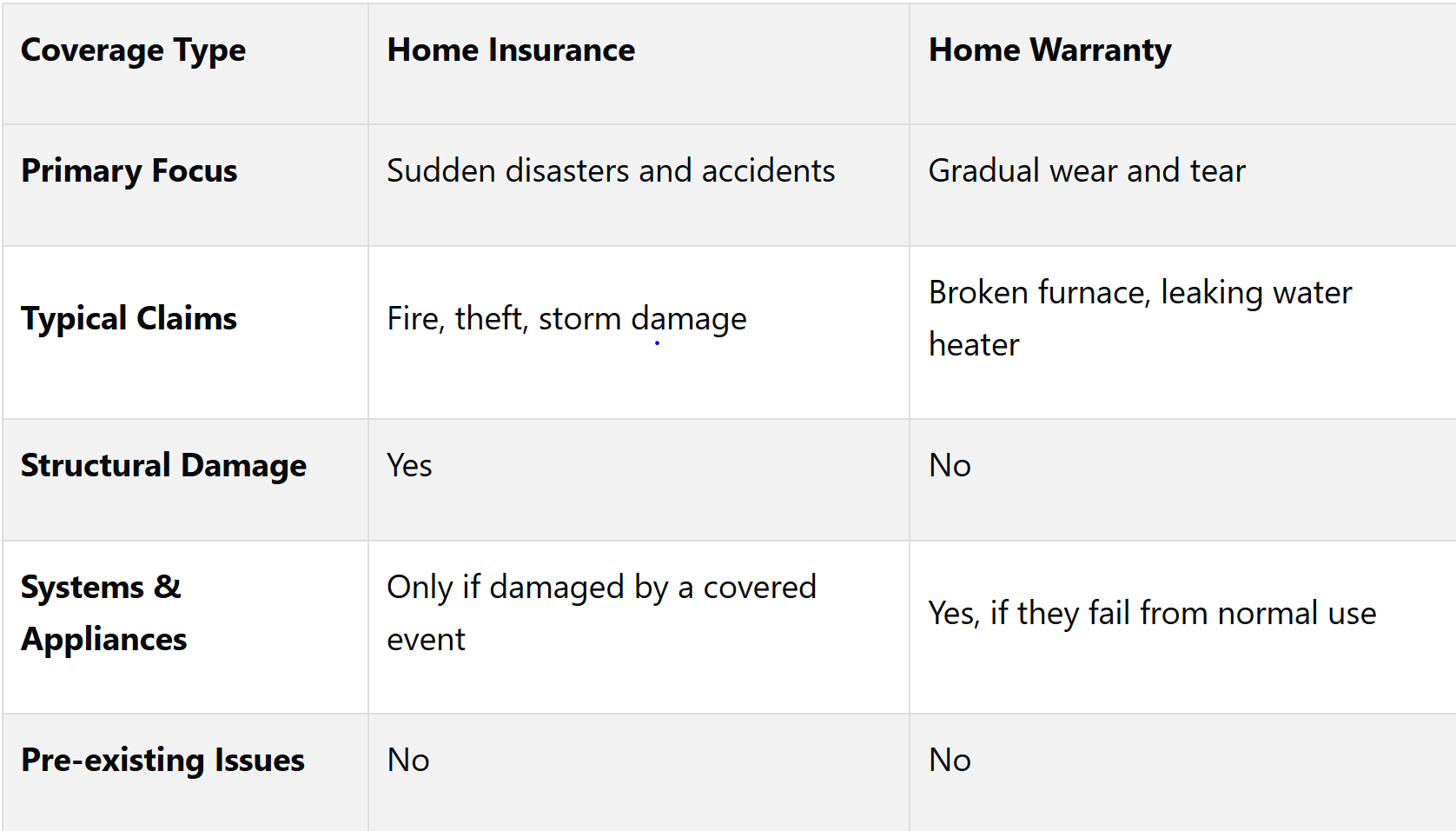

Understanding what each type of coverage offers can help you avoid unexpected expenses. While both home insurance and home warranties assist with home-related costs, they address very different issues.

Home Insurance Coverage Details

Home insurance is designed to protect you from sudden, costly disasters. It typically covers your home's structure, personal belongings, liability, and additional living expenses.

Structural coverage applies to damage caused by events like fire, theft, vandalism, windstorms, hail, lightning, and certain natural disasters [5]. For instance, if a windstorm damages your roof, your home insurance can help cover the repair or replacement costs.

It also covers personal property if it’s stolen or damaged and provides liability protection if someone gets injured on your property or if you’re held responsible for property damage. Additionally, if a covered event makes your home uninhabitable, home insurance can help pay for temporary housing and meals [5].

However, home insurance has its limits. It doesn’t cover wear and tear, maintenance issues, or damage from floods, earthquakes, or neglect [7]. For example, if your 15-year-old water heater stops working, it’s considered normal wear and tear, which falls outside the scope of home insurance.

Home Warranty Coverage Details

Home warranties focus on repairs or replacements for major systems and appliances that fail due to normal use [2]. This includes systems like HVAC, plumbing, and electrical setups, as well as appliances such as refrigerators, ovens, dishwashers, washers, and dryers.

Unlike home insurance, warranties are specifically designed to handle gradual wear and tear. According to industry data, home warranty claims are more frequent but usually involve lower costs, with service call fees ranging from $75 to $150 per visit [1]. However, warranties come with exclusions - they don’t cover structural elements like walls or roofs, pre-existing conditions, improper installations, or items that haven’t been properly maintained. Cosmetic issues and weather-related damage are also not included.

Main Coverage Differences

The key distinction lies in the cause and timing of the issue. Home insurance addresses sudden, unexpected events that cause immediate damage, whereas home warranties cover the gradual breakdown of systems and appliances over time.

For example, if a kitchen fire damages your cabinets and refrigerator, home insurance would cover the structural repairs and might also replace the refrigerator, as the damage was caused by a sudden event [5]. On the other hand, if your refrigerator stops working because of a worn-out compressor, a home warranty would step in, as this is a result of regular use [2].

These differences highlight why many homeowners choose to have both types of coverage. Home insurance provides a safety net for large, unexpected financial risks, while a home warranty helps manage the smaller but inevitable repair costs that come with owning a home. Together, they offer a more comprehensive approach to protecting your investment.

Cost Analysis: Home Insurance vs. Home Warranty Expenses

Now that we've covered the differences in coverage, let's dig into the costs associated with home insurance and home warranties. Breaking down these expenses can help you figure out which option - or combination - fits your financial plan.

Home Insurance Costs

Home insurance premiums usually fall between $610 and over $6,000 per year, with most homeowners paying somewhere in the range of $1,200 to $2,000 annually [2][3]. The cost of your premium is closely tied to your property's value - higher-value homes require more coverage, which drives up the cost. Additionally, location matters. Homes in disaster-prone or coastal regions tend to have higher premiums.

You’ll also need to consider deductibles, which are the out-of-pocket costs you pay before your insurance kicks in. Deductibles typically range from $500 to $2,500 per claim [2]. A higher deductible can lower your yearly premium, but it also means paying more if you file a claim. Many homeowners find a $1,000 deductible strikes a good balance between saving on premiums and keeping costs manageable when claims arise.

Home Warranty Costs

Home warranties, on the other hand, tend to have more predictable pricing. Annual costs usually range from $540 to $1,400, with most plans priced between $564 and $984 per year [1][2]. If you prefer monthly payments, expect to pay between $47 and $82 [1].

The type of plan you select impacts the cost significantly. Plans that cover only appliances or systems are often cheaper (around $400 to $600 annually), while broader plans that include both systems and appliances can go up to $1,400 or more [1][6]. Service fees, which you pay each time a technician visits, typically range from $70 to $150 [1][6][4]. Unlike insurance deductibles, these fees apply to every service call, no matter the repair cost.

Here’s a look at how some major providers stack up in 2025:

- American Home Shield: $36–$100 monthly ($426–$1,205 annually), with service fees of $100–$125 [1].

- Choice Home Warranty: $60–$68 monthly ($695–$792 annually), with a $100 service fee [1].

- Elite Home Warranty: $47–$60 monthly ($564–$720 annually), with service fees between $70 and $150 [1].

- AFC Home Warranty: $44–$82 monthly ($481–$904 annually), with service fees of $75–$125 [1].

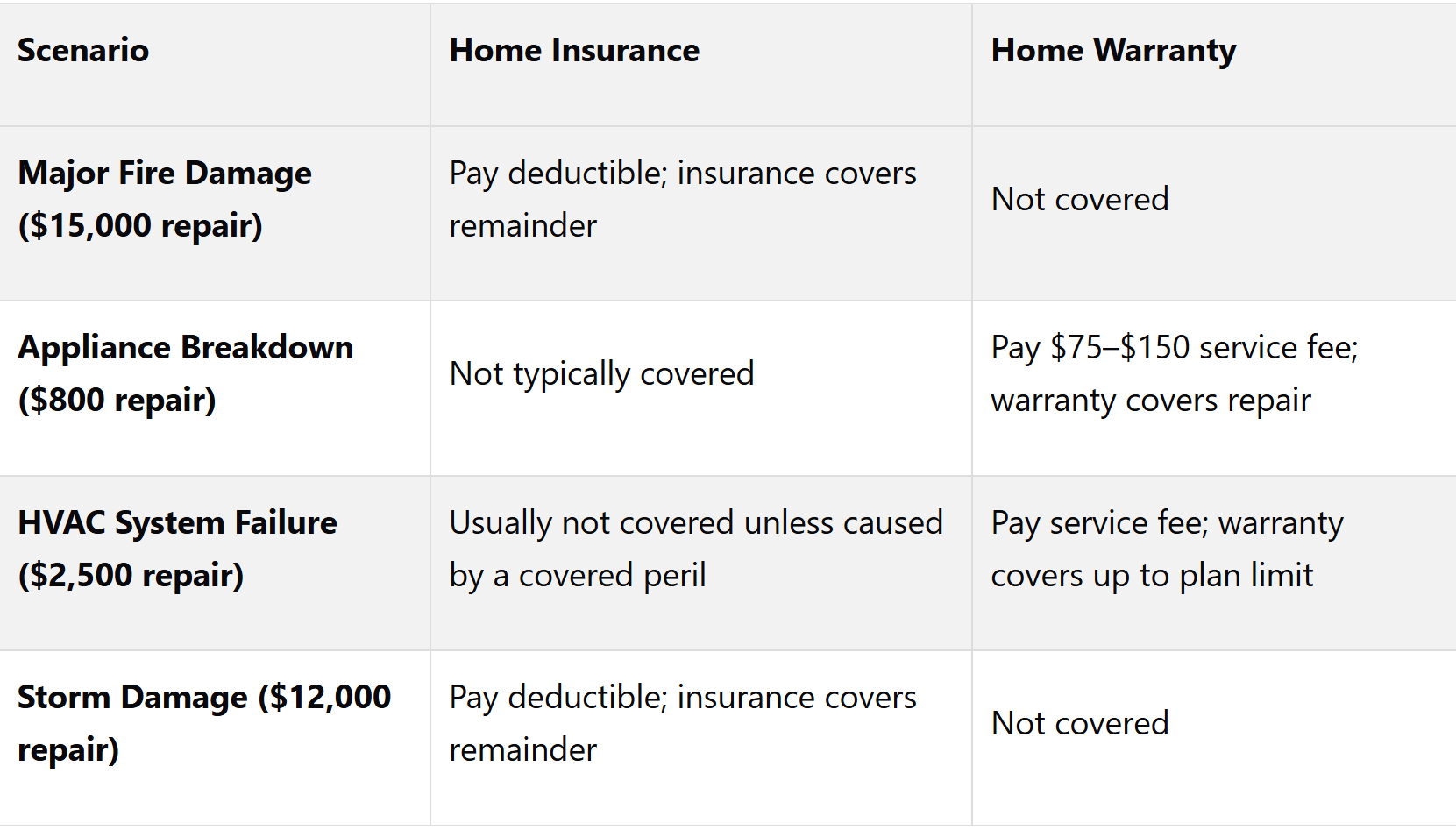

How Claims Work and Their Financial Effects

Knowing how to file claims and understanding potential out-of-pocket costs can give you a clearer picture of the financial impact of home insurance versus home warranties. The claims process varies significantly between the two, which directly affects costs. Let’s break it down, starting with home insurance.

Home Insurance Claims Process

When you need to file a home insurance claim, the first step is to notify your insurer as soon as possible after a covered event. You'll need to provide thorough documentation, such as photos, receipts, and an itemized list of damages. Depending on the severity, an adjuster may inspect your property.

Once your claim is approved, you’ll pay your deductible (e.g., $1,000 for a $10,000 loss), and your insurance will cover the remaining amount [2][5]. The timeline for payouts can range from a few days to several weeks, depending on how complex the claim is and whether further investigation is required.

On the other hand, home warranties simplify the repair process, making it quicker and less complicated.

Home Warranty Claims Process

If a covered appliance or system breaks down due to normal wear and tear, you contact your home warranty provider. They will arrange for a technician to assess and repair the issue [4][7]. This process is generally faster and more straightforward than filing a home insurance claim.

You’ll pay a service fee, typically between $75 and $150, for each visit [4][7]. For example, if your water heater breaks and the repair costs $1,000, you only pay the service fee, while the warranty covers the rest up to your plan's coverage limit. Repairs are often scheduled within a few days, although availability of technicians or parts can sometimes cause delays.

Financial Impact Comparison

The financial differences between home insurance and home warranties become clear when you compare how they handle various situations. Home insurance is designed to protect against significant, unexpected losses, offering substantial coverage once you meet your deductible [2][4][7]. In contrast, home warranties are better suited for routine repairs, keeping your out-of-pocket expenses limited to a predictable service fee [2][4][7].

Each option has its challenges. Home insurance claims can be denied or reduced if the damage results from lack of maintenance, excluded perils, or insufficient documentation [4][7]. Similarly, home warranty claims may be denied for pre-existing issues, improper maintenance, or if the item isn’t included in your contract [4][7].

Which Option Saves You More Money?

Deciding whether home insurance, a home warranty, or a combination of both saves you the most money depends on your specific circumstances. Understanding what drives the cost-effectiveness of each option can help you make a well-informed choice.

What Influences Cost-Effectiveness

The age and condition of your home play a major role. If you live in an older home with aging systems and appliances, a home warranty might be appealing. For example, replacing a major appliance like an HVAC system or refrigerator can cost anywhere from $1,500 to $5,000. In such cases, a home warranty could pay off if you face even one significant repair in a year [3].

Your local risk factors also matter. If your home is in an area prone to natural disasters, strong insurance coverage is essential, as the potential losses from events like hurricanes or wildfires can far outweigh the cost of annual premiums. On the other hand, a home warranty might save you hundreds or even thousands of dollars on repairs or replacements for issues like HVAC failures caused by normal wear and tear (after paying a service fee) [1] [6].

If you have limited emergency savings, a home warranty’s predictable annual cost and lower service fees can be attractive. In contrast, home insurance premiums can vary based on your claims history and local risks [3].

The frequency and size of claims are another key factor. Home insurance claims are less frequent but tend to involve large sums - often exceeding $10,000 for events like fire or storm damage [2]. Home warranty claims, on the other hand, are more common but typically cover smaller repairs or replacements, ranging from $200 to $2,000 per incident, plus a service fee [1] [3] [6].

Deductibles also differ. Home insurance deductibles are usually higher, starting at $1,000 or more per claim, meaning you’ll pay more out-of-pocket before coverage kicks in [2]. Home warranty service fees are lower, typically between $75 and $125 per service call, though you might incur these fees more often for smaller repairs [1] [3] [6].

These factors highlight why combining both options may offer the best financial protection.

Why Combining Both Can Be Beneficial

Given these cost considerations, many homeowners find that pairing home insurance with a home warranty provides well-rounded protection - especially for older homes or when emergency savings are tight [2] [3] [7]. This combination can shield you from both catastrophic events and the routine expenses of home maintenance.

Having both is particularly useful for older homes with aging systems, first-time homeowners who may not be prepared for maintenance costs, or those living in areas with high disaster risks and frequent appliance breakdowns [2] [3] [7]. Relying solely on home insurance leaves you vulnerable to out-of-pocket expenses for wear-and-tear-related breakdowns [2] [3]. On the flip side, depending only on a home warranty won’t protect you against major disasters like fires, theft, or severe weather events, which could lead to devastating financial losses [2] [3] [4].

Final Thoughts: Making the Right Choice

When deciding on coverage, it’s all about finding the right balance between risk, repair frequency, and cost predictability. The best choice depends on the benefits of each option and what your home truly needs.

Home insurance is designed to protect you from major, unexpected events like fires, storms, or theft. On the other hand, home warranties focus on wear-and-tear repairs for appliances and systems. Insurance claims often involve more paperwork and longer processing times, while warranty claims are typically simpler - just call for service, pay the fee, and get the issue fixed. However, warranties do come with limits and exclusions that might catch you off guard if you’re not familiar with the fine print.

The age and condition of your home and appliances play a key role in this decision. For newer homes with appliances still under manufacturer warranties, a home warranty might not add much value. But if you’ve got an older HVAC system or a water heater nearing the end of its lifespan, a warranty could save you thousands in repair or replacement costs.

For many homeowners, a combination of both insurance and a warranty works well. This approach helps reduce out-of-pocket expenses in different scenarios, offering comprehensive protection.

Another way to stay on top of costs is by organizing your records digitally. Tools like HouseFacts can simplify this process by tracking maintenance records, comparing coverage options, and spotting overlapping protections that might be costing you extra. With platforms like these, you can avoid redundant coverage and missed maintenance tasks that could void claims, ultimately saving you money.

Home insurance is non-negotiable - it’s often a lender requirement and provides essential financial protection. Home warranties, while optional, can be a smart choice for older homes or for those who prefer predictable repair costs over unexpected surprises.

Before making a decision, take a close look at your home’s age, the risks in your area, and the details of the coverage you’re considering. By weighing costs and claims processes carefully, you can tailor your coverage to suit your home’s needs and your financial situation. Combine that with effective digital tracking, and you’ll be ready to handle any home-related expense with confidence.